Table of Contents

- Why Set Goals? The Psychological Benefits

- Define Your Personal Values

- Understand Your Retirement Philosophy

- Make Your Goals SMART

- Estimate Your Spending Power

- Categorize Your Goals: Essential Needs, Flexible Wants, Legacy Wishes

- Lean on 4 Pillars to Support Your Goals

- Recognize the Implicit Goals Guiding You

- The Bottom Line: Values-Driven Goals Lead to Relaxed Confidence

Retirement opens up a whole new world of possibilities - finally, the chance to pursue those passions you've daydreamed about, and discover new meaning after so many years of routine. But without defining crystal clear goals rooted in your deepest values, retirement can quickly begin to feel aimless.

Anchoring your aspirations to your inner compass provides much-needed direction. And planning your days around your principles promises deep fulfillment.

I'll never forget this one couple I worked with some years back, Sharon and Alexander. They both shared this tremendous love of sailing - it was their biggest passion in life. Their core values centered on adventure, exploring to the farthest corners of the globe, and exposing their teenage son to diverse cultures before he grew up. Together we carved out an intentional goal of them sailing clear around the world as a family.

By first taking the time to clarify Sharon and Alexander's deepest values, I was able to help construct a tailored financial plan to fully fund this dream voyage of theirs through strategic bond investments and other approaches. Today, Sharon, Alexander, and their son are out sailing across the vast Pacific Ocean, living out such a meaningful retirement goal completely aligned with what they value most in this life.

Examples like Sharon and Alexander make crystal clear why intentional goal-setting is so vital for an engaged, fulfilling retirement. Defining goals rooted authentically in your most cherished values has been proven to instill relaxed confidence for the unknown journey ahead. By following the steps outlined here by our team, you too can find your own true north.

Why Set Goals? The Psychological Benefits

Many reach retirement after years of determined saving into vehicles like 401(k)s and IRAs. But now comes a shift - from the accumulation mindset to purposeful "decumulation" in retirement.

Just as intentional savings grew your assets, intentional spending can now fund your lifestyle.

However, without clearly defined objectives, retirement's endless possibilities feel aimless and out of reach.

Goals provide the psychological benefits of clarity, purpose, and direction - like a compass for a sailor.

Setting intentional goals prevents restlessly drifting through open days. Goals create focus amid limitless options, clarifying priorities. Defining goals makes time feel precious again when each day has a purpose.

Milestones mark progress, creating inherent fulfillment. Goals provide motivation even in retirement's headwinds, affirming you are on course.

So, how does one determine the right goals for a fulfilled retirement?

The process begins by precisely identifying personal values - the principles underlying who you are. Clarifying your values provides direction when you come to a fork in the road.

Define Your Personal Values

Your core values provide a compass to set meaningful goals aligned with your ideal retirement. Values reflect timeless principles guiding priorities and decisions.

While values may overlap, how they are prioritized differs for each person. For you, core values may include compassion, connection, creativity, or financial stability. Defining values precisely separates surface desires from bedrock meaning.

Values shape goals and daily choices. Finance-specific values like avoiding debt or saving diligently inform retirement aims. Sharon and Alexander valued cultural exploration with family. This led them to set a goal of sailing around the world before their son reached adulthood.

Here's a simple yet powerful values identification activity to try:

Make a list of the values most meaningful to you – things like family, spirituality, generosity, learning, etc. Really dig deep here.

Review your list closely and highlight the 5-7 core values holding the absolute most significance for you.

For each selected value, take a minute to write 1-2 sentences explaining why it's so important and what it means to you specifically.

Finally, rank these clarified values in order of priority for you.

I've created a video series sharing how successful retirees align their finances with their values, if you'd like to explore this topic further.

Regularly revisiting this type of reflection keeps your values vitalized as life inevitably evolves.

Most importantly, defining goals focused on your authentic values creates a purposeful, engaged retirement.

Observe your behaviors through the lens of your values.

Ask yourself - does generosity lead me to volunteer often?

Do relationships anchor my most memorable family trips?

Does attaining financial stability drive me to save diligently?

Clearly articulating your values provides direction when setting aligned goals and making major daily decisions. Your values become guideposts leading toward the retirement life you truly envision.

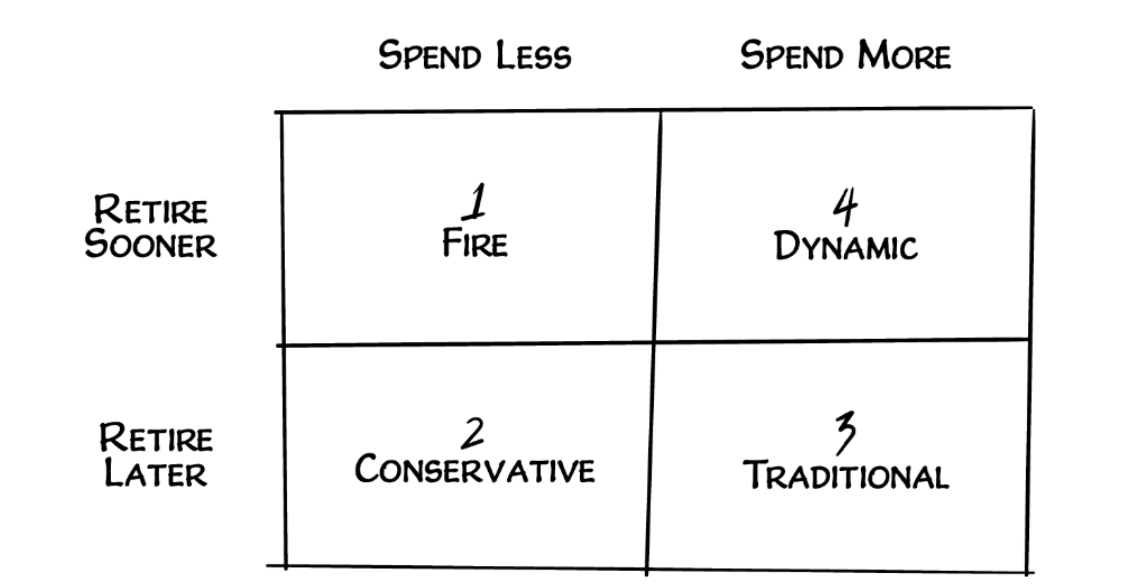

Understand Your Retirement Philosophy

Your retirement philosophy represents your viewpoint on how to approach your later years. It encompasses perspectives on spending, work/leisure balance, investing, and adventure.

Consider which philosophy best aligns with your values and vision:

FIRE – "Financial Independence, Retire Early" focuses on maximizing investments to enable early retirement, often by your 40s. This path resonates with those valuing freedom and frugality over work and spending. However, extreme saving may involve sacrifices. Carefully evaluate if this rigorous approach suits your values.

Conservative – This philosophy emphasizes preserving assets and generating low-risk income streams, often necessitating working into your 70s. The trade-off is enhanced security later, though potentially at the cost of pursing passions sooner. This approach resonates with those prioritizing stability.

Traditional – Working until your 60s and smoothly maintaining your pre-retirement lifestyle defines this path. It enables predictability by following conventional wisdom around retirement saving and investing. This philosophy fits those valuing continuity.

Dynamic – Regularly alternating work and leisure activities as interests evolve characterizes this philosophy. It provides flexibility to pursue new directions, but requires financial buffers to pivot. This resonates with those who embrace change.

Please note - there is no "right" answer.

Rarely does one philosophy perfectly capture an individual's perspective. Consider your values and shape a personalized hybrid philosophy guiding your vision. Then, set aligned goals and work backwards to make this retirement blueprint a reality.

While these philosophies present distinct approaches, you need not adhere rigidly to just one. Elements from multiple philosophies may resonate with your values and vision.

For example, you may aim to retire early, aligning with FIRE, but intend to work part-time in retirement for fulfillment rather than solely maximizing leisure. This balances the FIRE and Traditional philosophies.

Or you may plan to retire at a traditional age but sustain a more dynamic and flexible approach to work and spending in retirement. This blends Traditional and Dynamic elements.

Make Your Goals SMART

With values clarified and philosophy aligned, make goals SMART.

SMART is a powerful acronym for the five elements that strengthen retirement goal-setting:

Specific – Precisely define the goal details like what, why, who, when, and how. Vague goals breed confusion. Clearly articulating the specifics creates focus.

Measurable – Include quantifiable targets and metrics to tangibly measure progress. Defining numerical milestones enables tracking achievement.

Achievable – Ensure the goal is realistically feasible given your circumstances. Align goals with your skills, resources, and retirement timeline.

Relevant – Confirm the goal aligns with your values and retirement philosophy. Goals resonating with your core principles inspire follow-through.

Time-bound – Set a defined timeframe, including both a start and end date. A timeline generates urgency and prompts action.

Constructing SMART goals translates vague aspirations into defined roadmaps. Plans become actionable through clarity on specifics, metrics, alignment, and deadlines.

For example, saying "I want to launch a consulting practice" lacks essential details.

In contrast, here is a SMART goal:

"I will launch a marketing consulting practice by Q1 next year. Acquire 5 clients and generate $3,000 in monthly revenue within the first 12 months."

The above example defines an aim incorporating all 5 SMART elements. Such rigor provides clarity on how to achieve the goal. Progress tracking becomes possible through defined metrics. Milestones mark the path forward.

Applying the SMART framework lends focus so you can proactively pursue goals rather than drifting aimlessly. SMART goals power purposeful retirement.

Estimate Your Spending Power

Before detailing comprehensive goals, estimate your spending ability. The 4% rule provides a great starting point, but there's more to it than that. Here's how it works:

Total your retirement portfolio value

Multiply this sum by 4% to estimate initial sustainable yearly spending

For example, a $1 million portfolio suggests $40,000 first-year spending. Subsequently, increase yearly withdrawals by inflation while sustaining the portfolio.

This 4% guideline establishes your preliminary "Needs" spending capacity for core essentials like housing, utilities and food. As you shape goals, sculpt "Wants" and "Wishes" accordingly.

Remember, the 4% rule has important caveats:

It assumes withdrawal amounts are after advisory fees and before taxes. Budgeting only 4% could leave you short.

Other income like pensions and Social Security expands your spending potential beyond 4%.

Those retiring early may need to use portfolio funds as an income bridge until claiming Social Security.

Market returns do not always adhere to historical averages. Flexibility helps respond to volatility.

With a back-of-the-envelope spending estimate, thoughtfully define aims across needs, wants, and wishes.

Categorize Your Goals: Essential Needs, Flexible Wants, Legacy Wishes

Categorizing retirement goals into Needs, Wants, and Wishes is a core tenet of our planning process. This framework underpins our approach because each spending category aligns with a different funding source, enabling comprehensive financial plans.

Let's explain each category:

Needs - Non-discretionary spending for basic living expenses and healthcare. Needs are essential costs you must afford for life. They form the foundation enabling all other goals.

Wants - Discretionary spending that adds comfort and joy, like vacations, hobbies, and entertainment. Wants are flexible - they can adapt to market volatility if needed.

Wishes - Funds allocated toward legacy for heirs, causes you believe in, and the world beyond you. Wishes enable meaningful goals like charitable giving.

Needs are funded by guaranteed income sources like pensions to create a secure income floor.

Wants are supported through balanced investment portfolios aimed at growth.

Wishes are made possible by protecting and preserving wealth through legacy planning.

Defining goals within Needs, Wants, and Wishes identifies funding priorities.

Needs enable Wants, which permit Wishes.

Without covering Needs, other goals become impossible.

Wishes encompass aspirational legacy goals beyond just leaving an inheritance for your heirs. Wishes could fund grandchildren's education, charitable giving, or leaving a living legacy by starting an organization. Clarifying Wishes separates short-term Wants from deeper, more meaningful aspirations for multi-generational impact.

Lean on 4 Pillars to Support Your Goals

Bringing your retirement goals to life requires planning across four key pillars working in harmony:

Guaranteed Income – Make sources like pensions, Social Security, and annuities the core to cover essential spending needs. This enables confidently pursuing additional goals.

Strategic Investing – Invest surplus assets beyond guaranteed income into a tax-efficient, diversified portfolio designed to fund your wants and wishes.

Tax Minimization – Be proactive in minimizing taxes that could inhibit aims through asset location, structured withdrawals, and strategic gifting. Consult an expert for guidance.

Risk Mitigation – Identify key risks that could derail plans and insure what you cannot personally bear. This contains costs and provides stability.

For example, guaranteed income covering needs may allow more aggressive investing to fund wishes. Or insuring costly wishes may warrant higher premiums than flexible wants. Coordinate efforts based on your categorized goals.

These four pillars provide the framework for Clark Asset Management to custom-tailor financial plans around your unique goals. Our integrated process aims to provide relaxed confidence.

Recognize the Implicit Goals Guiding You

In addition to your explicit aims, reflect on unspoken goals shaping your path. These could look like:

Preserving assets to pass on

Maintaining lifestyle continuity

Retaining reserves to navigate pivots

Enjoying hard-earned leisure time

You may not have explicitly stated "leave an inheritance for heirs" as a goal. However, protecting wealth to pass on likely implicitly guides financial decisions. Making this intent intentional can focus on efficient planning.

Or perhaps guaranteed income covers your basic needs, allowing lavish vacations. But an implicit goal of maintaining financial flexibility to handle surprise costs may go unmet without conscious effort. Articulating the unspoken creates balance, and makes your plan that much more powerful.

The Bottom Line: Values-Driven Goals Lead to Relaxed Confidence

When goals steer each day toward purpose, retirement becomes your true north. Defining aims rooted in your values liberates potential. Pursuing passions breeds contentment.

Yet, few reach this destination alone. If you find yourself adrift, ask:

Are my goals aligned with my values?

Have I planned holistically to achieve them?

What trade-offs make goals attainable?

For a deeper exploration of these retirement planning concepts, you might find some valuable insights in 'Be The Bird.'